What Is an Asset?

An asset is a resource owned by an individual or organization which provides economic value.

This includes cash, equipment, property, rights, or anything that helps a company generate revenue or reduce expenses.

According to the International Financial Reporting Standards (IFRS), assets are obtained as a result of past transactions or events and are expected to provide future economic benefit, whether directly or indirectly.

For instance, a piece of equipment may be used to indirectly generate revenue, while cash is a more direct source of value.

Assets are important because they are what businesses use to operate and generate a profit.

It is also one of the three concepts of the fundamental accounting equation, alongside liabilities and equity.

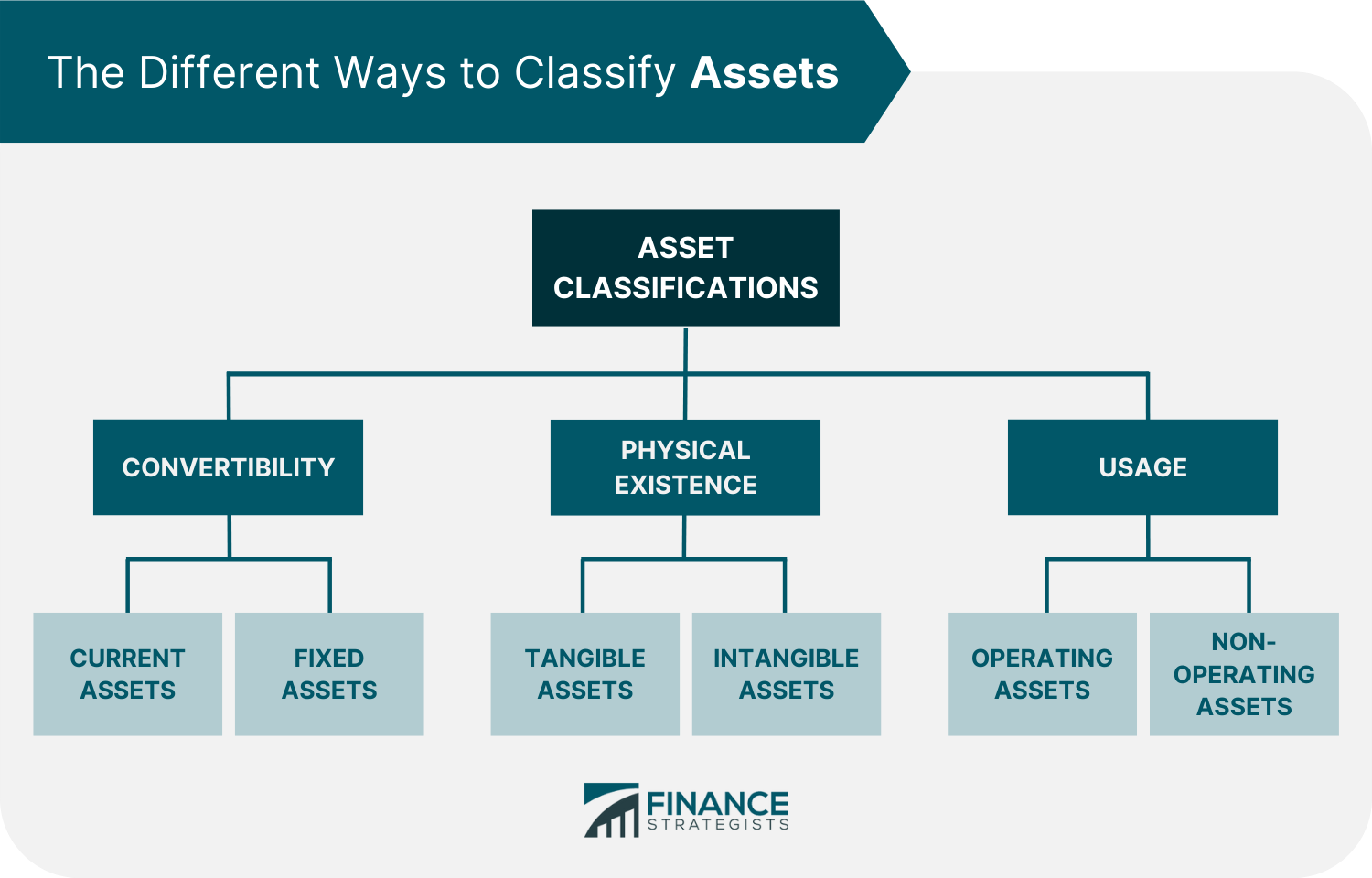

Classification of Assets

An asset can be classified in many different ways, usually involving its nature or purpose.

These are:

Convertibility

This classifies assets based on their liquidity or how easily they can be converted into cash.

Under this classification, assets are further subdivided into current assets and fixed assets.

Current Assets

Current assets are the most liquid type of assets and are expected to be consumed or converted to cash within one year.

Some examples of current assets include cash, short-term deposits, accounts receivable, prepaid expenses, inventory, and marketable securities.

Fixed Assets

Fixed assets are long-lived assets that cannot be easily and readily converted into cash or cash equivalents.

They are retained and expected to continue benefiting the business beyond a year.

Fixed assets are also referred to as noncurrent assets, long-term assets, or hard assets.

Some examples include land, building, and equipment.

Physical Existence

This classifies assets based on their material presence. In this classification, assets are either tangible or intangible.

Tangible Assets

Tangible assets are those assets that have a physical substance and are capable of being touched, felt, or seen.

Examples of such assets are equipment, cash, and inventory.

Intangible Assets

Resources with value but without physical substance fall into this category. These include patents, licenses, and copyrights.

Usage

This classifies assets based on their business operation usage or purpose.

Under this classification, assets are identified as being either operating assets or non-operating assets.

Operating Assets

Operating assets are necessary assets in the daily operation of a business.

They are used to generate revenue from the core business activities of a company.

Some examples of operating assets include cash, inventory, property, plant and equipment.

Non-Operating Assets

Non-operating assets are those assets that are not required for daily business operations.

Examples include fixed deposits, marketable securities, idle equipment, and vacant land.

Properties of an Asset

Assets have several important properties that make them valuable to businesses.

These include the following:

Ownership

An asset must be owned or controlled by an entity. It enables individuals and organizations to convert these assets into cash or cash equivalents and limits others from controlling or using them.

Assets can be leased but cannot be transferred or sold unless stipulated in the agreement.

For instance, a company may own a piece of land but lease the building on it.

Economic Value

Assets have value that can be measured in terms of cash or its equivalents. The measurement is generally done at the time of acquisition but can also be done at a later stage.

Assets are valued at either their historical cost or current market value. For instance, a company may have acquired a piece of machinery for $100,000 five years ago.

The current market value of the machinery may be $150,000. Using current market value is more common in financial reporting.

Resource

Assets are used in producing goods or services and generating income.

Thus, they can generate future economic value in the form of positive cash inflows.

Assets may also provide competitive advantage. For instance, a company may use its patents to produce new products which its competitors cannot.

Importance of Asset Classification

Below are some of the benefits of asset classification:

Provides an Overview of Financial Metrics

Classifying assets gives businesses an overview of their financial metrics, such as working capital and cash flow.

This information is important in deciding how to allocate resources and when to invest in new projects.

Estimates Solvency and Risk

Classifying assets also helps businesses estimate their solvency and risk. This is because different types of assets carry different levels of risk.

Assets such as commodities, currencies, and high-yield bonds carry risks because they have significant price volatility.

On the other hand, cash assets and money market funds are low-risk assets because they can withstand high levels of market volatility.

A company can mitigate these risks by diversifying its portfolio of assets.

Determines Contribution to the Business

Another benefit of asset classification is that it helps businesses to determine the contribution of each asset type, whether operating or non-operating, to generating revenue.

With this, companies can make more informed investment decisions which will improve their asset management.

How to Determine the Value of Assets

Businesses use different methods to determine the value of their assets.

The most common methods are the depreciation method, market value method, and standard cost method.

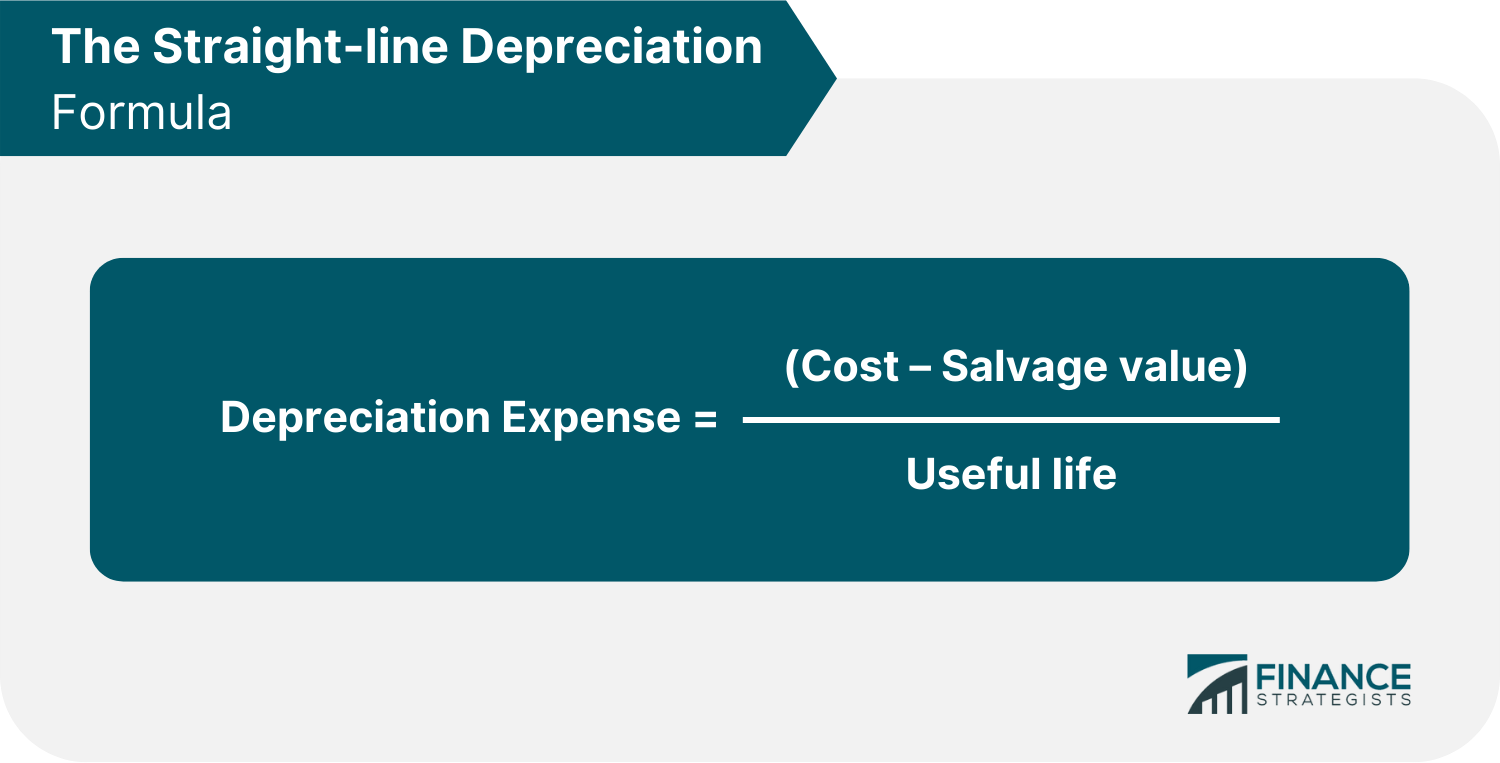

Depreciation Method

There are several methods for how to calculate depreciation. The most common methods are straight-line and double declining balance.

Straight-line Depreciation

The straight line is calculated by taking the original cost of the asset, making an allowance for what is known as a residual or salvage value and dividing it by the estimated useful life of the asset.

Below is the formula for the straight-line method of computing depreciation.

For instance, a company has a machine that costs $100,000. The salvage value is $5,000, and the useful life is five years.

Following the formula, the depreciation expense of the machine would be $19,000 per year.

Depreciation Expense = ($100,000 – $5,000) / 5 = $19,000 per year

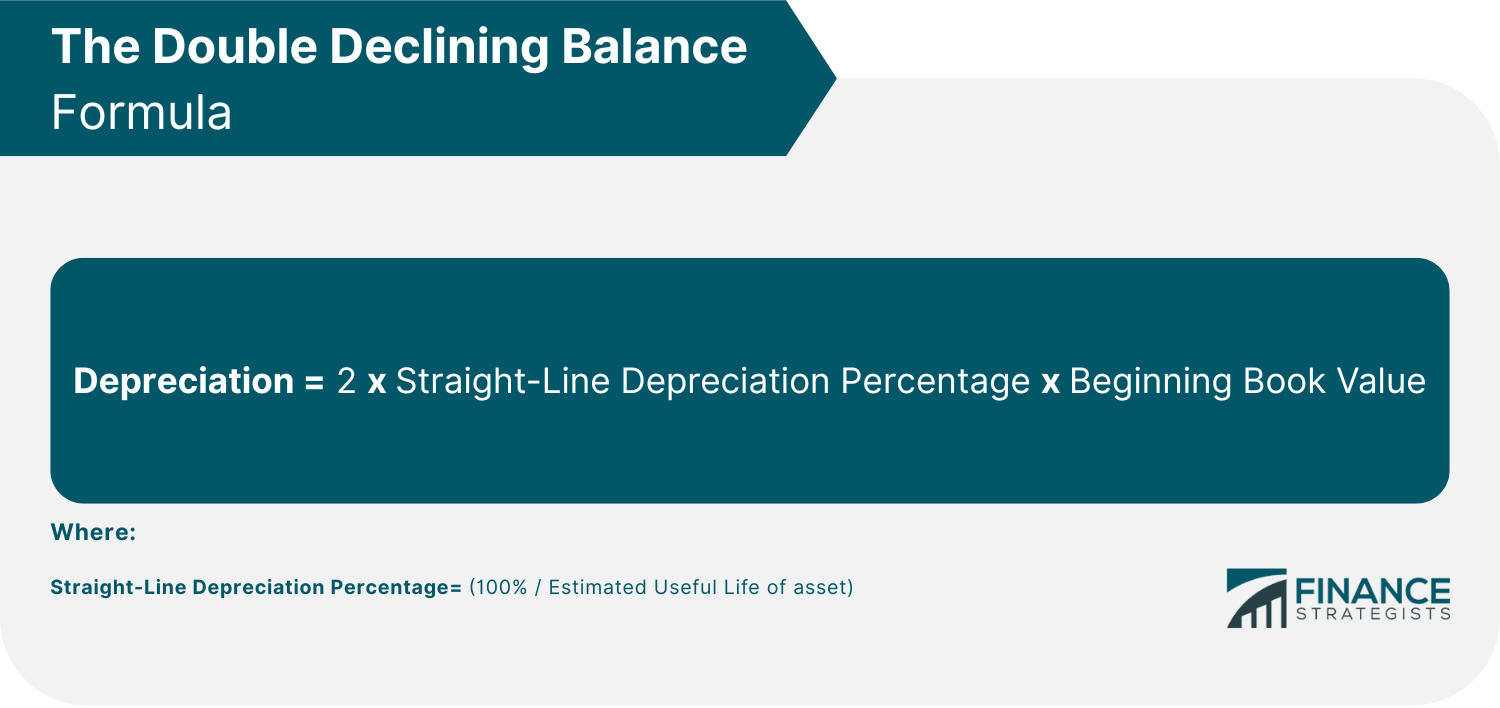

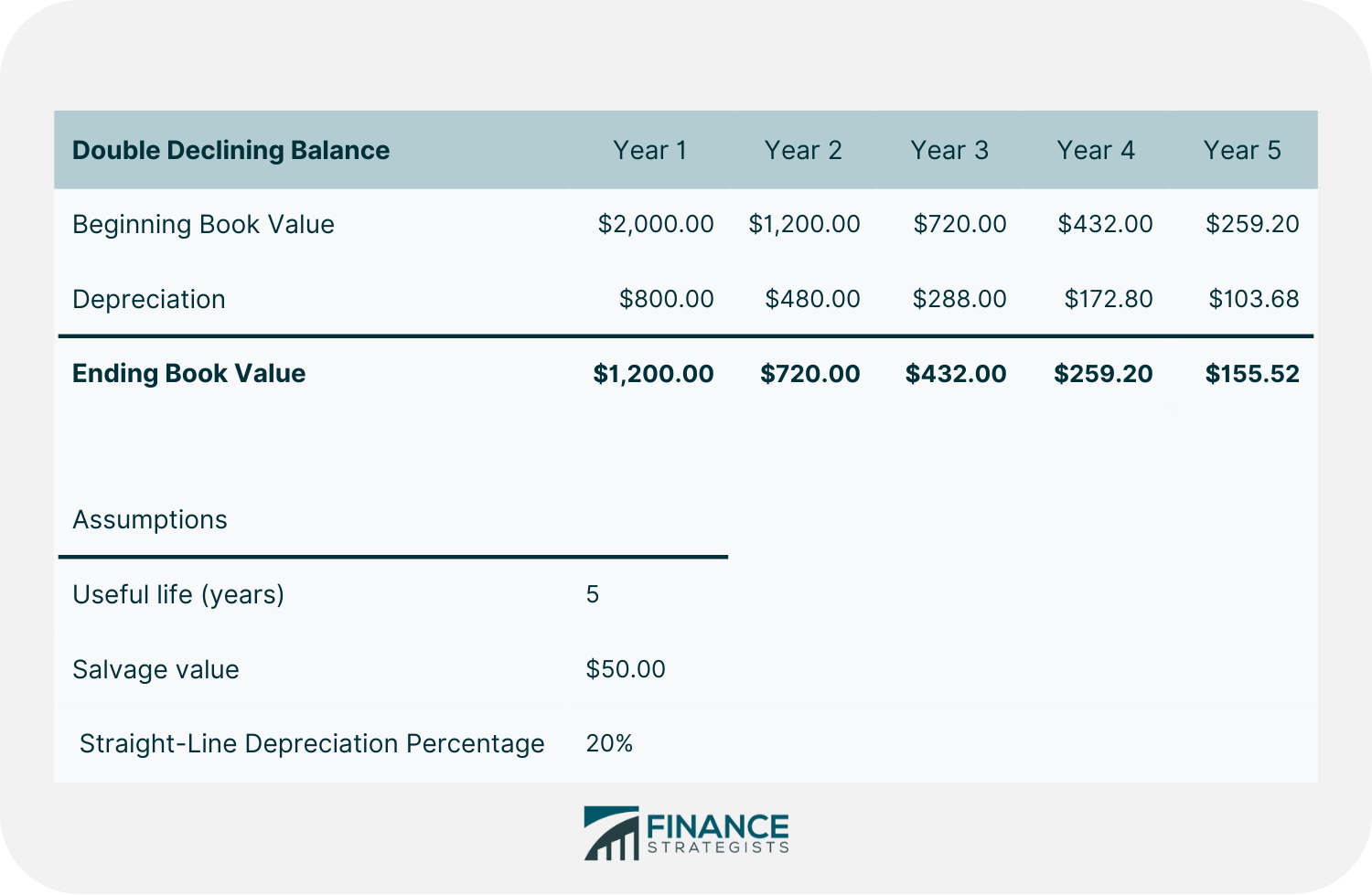

Double Declining Balance

Double declining balance considers higher amounts of depreciation in an asset’s early years as compared to its later years.

It reflects the fact that a lot of assets would be more productive when you first get them and then become less productive with time due to wear and tear.

The formula for double declining balance is as follows:

For example, a business purchased a machine for $2,000 with a salvage value of $50 and expected it to last for five years.

When applying the double declining balance method, the straight-line depreciation percentage is first calculated.

In this case, it would be 100% / 5 years of useful life or 20% per year.

Then it is doubled (20% x 2=40%). The resulting percentage is then deducted from each year of the asset’s useful life.

That would be 40% of 2,000 ($800) in year one, 40% of $1,200 ($480) in year two, and so on, stopping when the book value equals the salvage value.

Market Value Method

The market value method bases the value of an asset on the amount it might sell for in the marketplace.

It is the price the buyer is willing to pay the seller, assuming both have knowledge of the asset’s worth.

It also refers to the most recently quoted price for a market trade security or the value an investment community gives to a particular entity or business.

The fluctuation in supply and demand may influence market value.

For instance, a person is selling a house, and the market value is $500,000. If there are more buyers than sellers in the market, then the price of this house would go up.

Standard Cost Method

The standard cost method utilizes the expected costs of an asset instead of its actual costs.

This is often based on the past experience of a company, and it is determined by recording the difference between expected and actual costs.

This is done in cases where it might be too time-consuming to collect data for actual costs. Standard costs are used as a close estimate of actual costs instead.

Consequently, significant accounting efficiencies are created since standard costs usually only slightly differ from actual costs.

Asset vs. Liability vs. Equity

Asset, liability, and equity are the three largest classifications in every financial statement.

They comprise the main accounting equation and make up the balance sheet of a company.

Thus it is important to understand what differentiates each from the other.

To illustrate the difference between an asset, liability, and equity, let us consider this example.

You decide to buy a house for $500,000 and take out a loan or mortgage for the same amount in order to buy it.

Your home is an asset because it has value, and you can go to the market and sell it in exchange for cash. The loan is a liability because it is something you have to pay back.

Equity is the difference between assets and liabilities. Currently, your equity is zero because the value of these two are the same.

However, let us say that in five years, the value of your home appreciates to $600,000. This means that you have gained $100,000 in appreciation or value.

In the course of those five years, you pay down the mortgage from $500,000 to $400,000.

So your current equity is now $200,000 after subtracting liability from the value of your assets.

This means that if you liquidate your asset or sell your home for $600,000 and pay all of your mortgages for $400,000, this is how much cash you are going to have at the end of those transactions.

Therefore, equity tells you how much value you have in your home after paying off all of your liabilities.

The Bottom Line

Assets refer to anything that has economic value and can be converted into cash. They can be classified based on their convertibility, physical existence, or usage.

Assets also have three properties: ownership, economic value, and resource.

The value of assets can be determined through different methods, such as the depreciation method, standard cost method, and market value method.

Assets are different from liabilities and equity, which is important to understand for both personal finances and business accounting.

Assets are important to generate income and cash flow. Thus, it is essential to clearly understand how they can be used to make sound financial decisions.

Assets FAQs

Examples of assets include cash, investments, accounts receivable, inventory, land, and buildings.

Current assets are assets that can be easily converted into cash within one year. Fixed assets are long-term investments, such as land, buildings, and equipment, and are expected to provide benefits to the business beyond a year.

No. Labor is not an asset because it cannot be converted into cash. It is considered an expense. In particular, wages or salaries paid to employees are considered operating expenses.

Asset classification is important because it provides a clear overview of a company's financial position and helps in decision-making. It also helps businesses manage their resources more efficiently.

An asset is anything owned by an entity that has economic value and can be converted into cash. A liability is something that a business owes to another party.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.