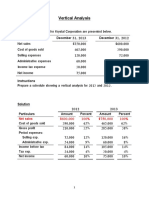

3 Cash Flows and Financial Analysis

3 Cash Flows and Financial Analysis

Download as pdf or txt

You might also like

- Internship ReportsDocument22 pagesInternship ReportsManoj ,100% (7)

- Offer Letter - Zaibunissa Naik - SDNA GlobalDocument4 pagesOffer Letter - Zaibunissa Naik - SDNA Globalzuber shaikhNoch keine Bewertungen

- Mayes 8e CH03 Problem SetDocument8 pagesMayes 8e CH03 Problem SetBunga Mega WangiNoch keine Bewertungen

- Financial Statement AnalysDocument68 pagesFinancial Statement AnalysDaisy GuiralNoch keine Bewertungen

- FinancialStmtAnalysis Garrison11ePPTDocument61 pagesFinancialStmtAnalysis Garrison11ePPTZeyadNoch keine Bewertungen

- AFM - Module 3Document61 pagesAFM - Module 3Abhishek JainNoch keine Bewertungen

- Financial Statement AnalysisDocument72 pagesFinancial Statement Analysis88ak07Noch keine Bewertungen

- Part 1 - Financial Statements AnalysisDocument38 pagesPart 1 - Financial Statements AnalysisAjmal KhanNoch keine Bewertungen

- "How Well Am I Doing?" Financial Statement AnalysisDocument61 pages"How Well Am I Doing?" Financial Statement AnalysisSederiku KabaruzaNoch keine Bewertungen

- Financial Statements AnalysisDocument35 pagesFinancial Statements AnalysisKiarra Nicel De TorresNoch keine Bewertungen

- Chap 014Document72 pagesChap 014Dimitris T. KonstantiosNoch keine Bewertungen

- Financial Accounting Fundamentals: John J. Wild 2009 EditionDocument57 pagesFinancial Accounting Fundamentals: John J. Wild 2009 EditionMariamiNoch keine Bewertungen

- Chapter 7 Financial Statments AnalysisDocument44 pagesChapter 7 Financial Statments AnalysisAddisalem MesfinNoch keine Bewertungen

- Financial Statement AnalysisDocument42 pagesFinancial Statement AnalysisMd IslamNoch keine Bewertungen

- Accounting & Finance (Session-7)Document60 pagesAccounting & Finance (Session-7)Ibrahim QariNoch keine Bewertungen

- Financial Statement AnalysisDocument53 pagesFinancial Statement AnalysisSameh YassienNoch keine Bewertungen

- Financial Statement AnalysisDocument48 pagesFinancial Statement AnalysisCheryl LowNoch keine Bewertungen

- Chap 014Document73 pagesChap 014rikitagujralNoch keine Bewertungen

- Financial Statement Analysis DemoDocument51 pagesFinancial Statement Analysis DemoMylene SalvadorNoch keine Bewertungen

- Chap 2 Financial Analysis & PlanningDocument108 pagesChap 2 Financial Analysis & PlanningmedrekNoch keine Bewertungen

- Activity - Financial StatementsDocument5 pagesActivity - Financial StatementsPhilip Jhon BayoNoch keine Bewertungen

- Financial Statement AnalysisDocument31 pagesFinancial Statement AnalysisbilalahmedbhuttoNoch keine Bewertungen

- Unit 4. Financial Statement Analysis - Horizontal Analysis of Comparative Statement and Trend PercentageDocument23 pagesUnit 4. Financial Statement Analysis - Horizontal Analysis of Comparative Statement and Trend PercentageWoodsville HouseNoch keine Bewertungen

- Handout 7 - Business FinanceDocument3 pagesHandout 7 - Business FinanceCeage SJNoch keine Bewertungen

- Part G. Finance (2) - Lecture 8Document71 pagesPart G. Finance (2) - Lecture 8Elís RosanaNoch keine Bewertungen

- Cash Flow Analysis: Mcgraw-Hill/Irwin © 2004 The Mcgraw-Hill Companies, Inc., All Rights ReservedDocument27 pagesCash Flow Analysis: Mcgraw-Hill/Irwin © 2004 The Mcgraw-Hill Companies, Inc., All Rights Reservedmabkhan_25Noch keine Bewertungen

- 2023 - Session12 - 13 FSA2 - MBA - SentDocument32 pages2023 - Session12 - 13 FSA2 - MBA - SentAkshat MathurNoch keine Bewertungen

- Ch-2 Financial Analysis &planningDocument27 pagesCh-2 Financial Analysis &planningMulatu LombamoNoch keine Bewertungen

- Chapter 5Document23 pagesChapter 52t65xn9qqzNoch keine Bewertungen

- Financial Statements and Ratio AnalysisDocument26 pagesFinancial Statements and Ratio Analysismary jean giananNoch keine Bewertungen

- Detailed Analysis CfsDocument16 pagesDetailed Analysis CfsDhruv TrehanNoch keine Bewertungen

- Cash Flow StatementDocument22 pagesCash Flow StatementThe ONE GUYNoch keine Bewertungen

- CH 13Document4 pagesCH 13Sri HimajaNoch keine Bewertungen

- Financial Analysis LiquidityDocument22 pagesFinancial Analysis LiquidityRochelle ArpilledaNoch keine Bewertungen

- Financial Statement and Ratio AnalysisDocument182 pagesFinancial Statement and Ratio AnalysisAsad AliNoch keine Bewertungen

- Financial Analysis and InterpretationDocument22 pagesFinancial Analysis and Interpretationirfan_rana4uNoch keine Bewertungen

- FABM2-Chapter4 NDocument10 pagesFABM2-Chapter4 NArchie CampomanesNoch keine Bewertungen

- Fin Man - Intro To FsDocument16 pagesFin Man - Intro To FsdanicaNoch keine Bewertungen

- UntitledDocument5 pagesUntitledSophia Amrie Mendoza GarciaNoch keine Bewertungen

- CH03 ProblemDocument3 pagesCH03 Problemtrangtran01010Noch keine Bewertungen

- DauderisAnnand-IntroFinAcct-Chapter11 AmendedDocument15 pagesDauderisAnnand-IntroFinAcct-Chapter11 AmendedHome Made Cookin'Noch keine Bewertungen

- Horizontal & Vettical AnalysisDocument32 pagesHorizontal & Vettical Analysisela cagsNoch keine Bewertungen

- Contemporary Financial Management 10th Edition Moyer Solutions Manual 1Document15 pagesContemporary Financial Management 10th Edition Moyer Solutions Manual 1carlo100% (51)

- Chapter No 06 Final Afs-1Document58 pagesChapter No 06 Final Afs-1salwaburiroNoch keine Bewertungen

- Chapter 6 (CF)Document51 pagesChapter 6 (CF)Hossain BelalNoch keine Bewertungen

- Financial Ratio Analyses and Their Implications To ManagementDocument46 pagesFinancial Ratio Analyses and Their Implications To ManagementPrinsesa EsguerraNoch keine Bewertungen

- Understanding The FSDocument21 pagesUnderstanding The FSDivina Gammoot100% (1)

- Cash Flow Statement Illustration (IAS 7)Document2 pagesCash Flow Statement Illustration (IAS 7)amahaktNoch keine Bewertungen

- Fma 04Document38 pagesFma 04Zemenaye TsegayeNoch keine Bewertungen

- Analysis of Fianacial Statements-9Document25 pagesAnalysis of Fianacial Statements-9rohitsf22 olypm100% (1)

- Chapter 11 Notes (RJM) - BarrettDocument12 pagesChapter 11 Notes (RJM) - BarrettEmma DevineNoch keine Bewertungen

- Kelompok 6 - UTS AKMDocument18 pagesKelompok 6 - UTS AKM21-010 Desi MailaniNoch keine Bewertungen

- Vertical Analysis SolutionsDocument5 pagesVertical Analysis SolutionsSamer IsmaelNoch keine Bewertungen

- FIN 254 - Ratio Analysis NotesDocument52 pagesFIN 254 - Ratio Analysis Notestarek khanNoch keine Bewertungen

- Topic 2 Finance Ratios 1Document101 pagesTopic 2 Finance Ratios 1Lugan JacobNoch keine Bewertungen

- Chapter 6 For CUP Financial AccountingDocument15 pagesChapter 6 For CUP Financial Accountingratanak_kong1-9Noch keine Bewertungen

- Technopreneurship PPT Presentation Group 1Document57 pagesTechnopreneurship PPT Presentation Group 1Mia ElizabethNoch keine Bewertungen

- FS Analysis PDFDocument4 pagesFS Analysis PDFseraseraquexNoch keine Bewertungen

- Analysis and Interpretation of Financial Statements: Mgr. Andrea Gažová, PHDDocument33 pagesAnalysis and Interpretation of Financial Statements: Mgr. Andrea Gažová, PHDRoberto SanchezNoch keine Bewertungen

- Chapt 5 - Final Slides 2024Document48 pagesChapt 5 - Final Slides 2024notsonogNoch keine Bewertungen

- Chapter ThreeDocument71 pagesChapter Threeyared gebrewoldNoch keine Bewertungen

- Statement of Cash Flows: Preparation, Presentation, and UseFrom EverandStatement of Cash Flows: Preparation, Presentation, and UseNoch keine Bewertungen

- 4 Basics of Analysis - SeatworkDocument4 pages4 Basics of Analysis - SeatworkMarlon LadesmaNoch keine Bewertungen

- 1 Introduction To Financial Reporting and InformationDocument22 pages1 Introduction To Financial Reporting and InformationMarlon LadesmaNoch keine Bewertungen

- ACC117-CON09 Module 2 ExamDocument12 pagesACC117-CON09 Module 2 ExamMarlon LadesmaNoch keine Bewertungen

- 2 Statement of Financial PositionDocument51 pages2 Statement of Financial PositionMarlon Ladesma100% (2)

- ACC117-CON09 Module 3 ExamDocument16 pagesACC117-CON09 Module 3 ExamMarlon LadesmaNoch keine Bewertungen

- 1 Introduction To Financial ManagementDocument16 pages1 Introduction To Financial ManagementMarlon LadesmaNoch keine Bewertungen

- ACC117-CON09 Module 1 ExamDocument10 pagesACC117-CON09 Module 1 ExamMarlon LadesmaNoch keine Bewertungen

- 4 Financial Forecasting, Planning, and BudgetingDocument20 pages4 Financial Forecasting, Planning, and BudgetingMarlon LadesmaNoch keine Bewertungen

- 3 Cash Flows and Financial Analysis Seatwork With AnswersDocument6 pages3 Cash Flows and Financial Analysis Seatwork With AnswersMarlon LadesmaNoch keine Bewertungen

- 5 Time Value of MoneyDocument27 pages5 Time Value of MoneyMarlon LadesmaNoch keine Bewertungen

- Possibility of Ijma in Contemporary WorldDocument2 pagesPossibility of Ijma in Contemporary WorldFarah AthirahNoch keine Bewertungen

- Registration of Supplier and Contractors Fy23Document2 pagesRegistration of Supplier and Contractors Fy23munashe rayNoch keine Bewertungen

- Google Adwords Advanced Display Exam AnswersDocument97 pagesGoogle Adwords Advanced Display Exam AnswersCertificationAnswersNoch keine Bewertungen

- Cambridge International AS & A Level: Business 9609/12 March 2021Document16 pagesCambridge International AS & A Level: Business 9609/12 March 2021LisaNoch keine Bewertungen

- Yperfocus: How To Be More Productive in A World of DistractionDocument3 pagesYperfocus: How To Be More Productive in A World of DistractionSushant50% (2)

- Two Decades of Primary Dealer Operations in India: Sahana Rajaram and Payal GhoseDocument24 pagesTwo Decades of Primary Dealer Operations in India: Sahana Rajaram and Payal GhoseHetanshNoch keine Bewertungen

- OSA Sidomukti LestarDocument4 pagesOSA Sidomukti LestarBenny SembiringNoch keine Bewertungen

- DVC Tender PDFDocument51 pagesDVC Tender PDFchandan kumar SinghNoch keine Bewertungen

- Aggregate Planning, MRP Ch-3Document108 pagesAggregate Planning, MRP Ch-3Ayush SharmaNoch keine Bewertungen

- Settlement ManagementDocument6 pagesSettlement ManagementKarthik BhiravajoshulaNoch keine Bewertungen

- Five Small Bronze Hoards From Sardis and Their Implications For Coin Circulation in The Fifth Century C.E.Document21 pagesFive Small Bronze Hoards From Sardis and Their Implications For Coin Circulation in The Fifth Century C.E.Merve ToyNoch keine Bewertungen

- CONFERENCEDocument1 pageCONFERENCEKamboj BhartiNoch keine Bewertungen

- Valuation of CondominiumDocument19 pagesValuation of CondominiumRalph BacarNoch keine Bewertungen

- Tle 6 Ict Lesson 1Document5 pagesTle 6 Ict Lesson 1mary antonette colladoNoch keine Bewertungen

- Kurukshetra Financial Empowerment of Women 09-04-22Document4 pagesKurukshetra Financial Empowerment of Women 09-04-22avnishNoch keine Bewertungen

- SHINE CONTRACT-DilshaniDocument5 pagesSHINE CONTRACT-Dilshanimariyamshadha2Noch keine Bewertungen

- Consumer Protection Act 2019: July 20th 2020Document13 pagesConsumer Protection Act 2019: July 20th 2020Rohan GuptaNoch keine Bewertungen

- ASI Insurance PDFDocument5 pagesASI Insurance PDFSARDER JERIN SARAHNoch keine Bewertungen

- Financial Management - TVM Assignment 2 - Abdullah Bin Amir - Section ADocument4 pagesFinancial Management - TVM Assignment 2 - Abdullah Bin Amir - Section AAbdullah AmirNoch keine Bewertungen

- Memorandum Group 6Document15 pagesMemorandum Group 6Jewel JalataNoch keine Bewertungen

- Rating Action Moodys Downgrades Limas Rating 26may2023 PR 477088Document6 pagesRating Action Moodys Downgrades Limas Rating 26may2023 PR 477088Diario El Comercio100% (1)

- Quotation For Dough Sheeter MachineDocument6 pagesQuotation For Dough Sheeter MachinePereNoch keine Bewertungen

- Tugas 5 (Kelompok 5)Document9 pagesTugas 5 (Kelompok 5)Silviana Ika Susanti67% (3)

- Bosiet Quotation Bapak CokyDocument2 pagesBosiet Quotation Bapak CokyCoky Jamesta Kasih KasegerNoch keine Bewertungen

- Marketing FunctionsDocument25 pagesMarketing FunctionsSuny JubayerNoch keine Bewertungen

- Industrial Relations in Canada 3rd Edition Hebdon Solutions ManualDocument11 pagesIndustrial Relations in Canada 3rd Edition Hebdon Solutions ManualMarvinJonesdmyxa100% (11)

- Bentley RFP Project - VisonaryDocument15 pagesBentley RFP Project - Visonaryapi-543038192Noch keine Bewertungen

- Labor Law 1 PDFDocument129 pagesLabor Law 1 PDFirditchNoch keine Bewertungen