Download as pdf or txt

You might also like

- Abby Windows and Exteriors Sues Journo and 5 Employees For Exposing Corporate Corruption, Eavesdropping and Other AbusesDocument247 pagesAbby Windows and Exteriors Sues Journo and 5 Employees For Exposing Corporate Corruption, Eavesdropping and Other Abuseschristopher kingNo ratings yet

- Dave Banking Direct Deposit Enrollment FormDocument1 pageDave Banking Direct Deposit Enrollment FormDavid HannaganNo ratings yet

- City of Columbus Reaches Settlement Agreement With Plaintiffs in Alsaada v. ColumbusDocument2 pagesCity of Columbus Reaches Settlement Agreement With Plaintiffs in Alsaada v. ColumbusABC6/FOX28No ratings yet

- Ranco Costa Verda ContractDocument21 pagesRanco Costa Verda ContractGregory RussellNo ratings yet

- Kelli Prather ComplaintDocument16 pagesKelli Prather ComplaintSherry Turco CoolidgeNo ratings yet

- Criminal Complaint Against Alleged Rapist Jacob Blake of KenoshaDocument4 pagesCriminal Complaint Against Alleged Rapist Jacob Blake of KenoshaV SaxenaNo ratings yet

- Sabina Exconde Vs Delfin and Dante CapunoDocument2 pagesSabina Exconde Vs Delfin and Dante CapunoHoney Bunch100% (2)

- Eddie Tipton Lottery Charges Wisconsin - Dec. 22, 2016Document14 pagesEddie Tipton Lottery Charges Wisconsin - Dec. 22, 2016dmronline100% (1)

- Nicole Mitchell Criminal ComplaintDocument6 pagesNicole Mitchell Criminal ComplaintMark Wasson100% (1)

- SBA Offers Disaster Assistance To Businesses and Residents of Georgia Affected by Hurricane IdaliaDocument2 pagesSBA Offers Disaster Assistance To Businesses and Residents of Georgia Affected by Hurricane IdaliaSeth FeinerNo ratings yet

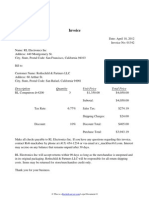

- InvoiceDocument1 pageInvoiceRocketLawyerNo ratings yet

- Cheque Clearing - An OverviewDocument20 pagesCheque Clearing - An OverviewGiridhaaran.VNo ratings yet

- File 3Document3 pagesFile 3Kimberly NugentNo ratings yet

- 2012 - Sierra County Property Tax Deadbeats!Document1,010 pages2012 - Sierra County Property Tax Deadbeats!Sophia PeronNo ratings yet

- How To Apply For Poor Person StatusDocument3 pagesHow To Apply For Poor Person Statusben realNo ratings yet

- Austin Hsu Complaint On COVID-related FraudDocument15 pagesAustin Hsu Complaint On COVID-related FraudGeekWireNo ratings yet

- Activate Your BPI Credit CardDocument3 pagesActivate Your BPI Credit CardAl Patrick Dela CalzadaNo ratings yet

- 2020 05-11-55 Order On Preliminary InjunctionDocument39 pages2020 05-11-55 Order On Preliminary InjunctionKUNC NewsroomNo ratings yet

- Dealers ComplaintDocument70 pagesDealers ComplaintGMG EditorialNo ratings yet

- KST803472586 Auth LetterDocument3 pagesKST803472586 Auth Letterreview bazaarNo ratings yet

- Cyber Creditcard System Synopsis This Creditcard Banking (CCB) Allows The User To Use His Credit CardDocument10 pagesCyber Creditcard System Synopsis This Creditcard Banking (CCB) Allows The User To Use His Credit CardMaadhuri KandrakotaNo ratings yet

- Criminal Cases JURISDICTIONDocument9 pagesCriminal Cases JURISDICTIONPeeve Kaye BalbuenaNo ratings yet

- Disaster Business Loan ApplicationDocument4 pagesDisaster Business Loan ApplicationalexNo ratings yet

- Georgia GatewayDocument4 pagesGeorgia GatewayEmmanuel MartinsNo ratings yet

- Former Director of Seattle Startup Accused of Embezzling $2M in Company FundsDocument15 pagesFormer Director of Seattle Startup Accused of Embezzling $2M in Company FundsGeekWireNo ratings yet

- Human Rights AlertDocument23 pagesHuman Rights AlertHuman Rights Alert - NGO (RA)No ratings yet

- Credit Card Authorization Form: Thomas A. KeelerDocument1 pageCredit Card Authorization Form: Thomas A. KeelerThomas KeelerNo ratings yet

- Twitter Argues Against Elon Musk's Plea To Schedule Trial in 2023Document10 pagesTwitter Argues Against Elon Musk's Plea To Schedule Trial in 2023Maria MeranoNo ratings yet

- 10-04-05 Top 10 Alleged Violations of Human Rights by The United States - Notice To The UN Hight Commissioner: Efforts To Undermine The 2010 Universal Periodic ReviewDocument9 pages10-04-05 Top 10 Alleged Violations of Human Rights by The United States - Notice To The UN Hight Commissioner: Efforts To Undermine The 2010 Universal Periodic ReviewHuman Rights Alert - NGO (RA)No ratings yet

- Mortgage Fraud Web Front Page 07-24-07Document4 pagesMortgage Fraud Web Front Page 07-24-07Houston Criminal Lawyer John T. FloydNo ratings yet

- 682928794-Jan-2023 2Document4 pages682928794-Jan-2023 2chde795No ratings yet

- Downloadable Bank Statement ExampleDocument5 pagesDownloadable Bank Statement ExampleJovica CaricicNo ratings yet

- TD Bank Penn Motor Sales Inc Apr-MayDocument3 pagesTD Bank Penn Motor Sales Inc Apr-Mayyusuf FajarNo ratings yet

- Are Prosecutors Immune From Lawsuits For Fabricating Evidence 0710Document7 pagesAre Prosecutors Immune From Lawsuits For Fabricating Evidence 0710sbhasin1100% (1)

- Cardholder Agreement Visa 637621Document8 pagesCardholder Agreement Visa 637621chrisNo ratings yet

- How To Get What The US Government Owes You!Document4 pagesHow To Get What The US Government Owes You!creativemarcoNo ratings yet

- Lab Req 11Document2 pagesLab Req 11karthick TNo ratings yet

- Inside CRDocument18 pagesInside CRheadpncNo ratings yet

- Credit OwnDocument1 pageCredit OwnLuis Miguel PedemonteNo ratings yet

- Defendant'S Motion To Dismiss With Prejudice For Lack of Probable Cause PlaintiffDocument3 pagesDefendant'S Motion To Dismiss With Prejudice For Lack of Probable Cause PlaintiffEvol LoveNo ratings yet

- Including The Long Form Fee Disclosure ("List of All Fees.")Document9 pagesIncluding The Long Form Fee Disclosure ("List of All Fees.")Shamara LoganNo ratings yet

- SMUD vs. Bank of AmericaDocument181 pagesSMUD vs. Bank of AmericaKathleenHaleyNo ratings yet

- Full Name in English Bank Name Ifsccode Account NumberDocument7 pagesFull Name in English Bank Name Ifsccode Account NumberVarun MarwahaNo ratings yet

- Teaching CertificateDocument1 pageTeaching Certificateapi-359162285No ratings yet

- Kroger Lawsuit Order Denying Motion To DismissDocument10 pagesKroger Lawsuit Order Denying Motion To Dismisspaula christianNo ratings yet

- Better Covid ThingDocument4 pagesBetter Covid ThingAuguste RiedlNo ratings yet

- Statement of Account: American Express® Platinum Travel Credit CardDocument5 pagesStatement of Account: American Express® Platinum Travel Credit Cardkumar kNo ratings yet

- View Paycheck: Employee InformationDocument4 pagesView Paycheck: Employee InformationJohn January0% (1)

- ForfeitureDocument34 pagesForfeiturerkarlinNo ratings yet

- Capital One CC Application Method @LarryLarrry05Document32 pagesCapital One CC Application Method @LarryLarrry05bryanclark0000100% (1)

- American Express Bank FSB V ZweigenhaftDocument9 pagesAmerican Express Bank FSB V ZweigenhaftKNo ratings yet

- Nevada Reports 1906-1907 (29 Nev.) PDFDocument420 pagesNevada Reports 1906-1907 (29 Nev.) PDFthadzigsNo ratings yet

- Abiola Folarin Apr 28 - May 29 BOA Bank StatementDocument12 pagesAbiola Folarin Apr 28 - May 29 BOA Bank StatementLillian AwtNo ratings yet

- Buy SSN NumberDocument7 pagesBuy SSN NumberBuy SSN NumberNo ratings yet

- Mariana & Others V (1) BHP Group PLC ( (2) BHP Group PLC A2021 0290 ADocument32 pagesMariana & Others V (1) BHP Group PLC ( (2) BHP Group PLC A2021 0290 AMArcela Gracie100% (1)

- 158664mastercard Gift Card Balance: Often Asked Questions Responded ToDocument5 pages158664mastercard Gift Card Balance: Often Asked Questions Responded Tot.u.an.p.ksd02No ratings yet

- HOTEL CC Authorization FormDocument1 pageHOTEL CC Authorization FormSacramento SirensNo ratings yet

- DS82 CompleteDocument6 pagesDS82 CompleteAjith PrasannaNo ratings yet

- Authorization Letter Sunday MorningDocument1 pageAuthorization Letter Sunday MorningHamad FalahNo ratings yet

- Colombia Check StubDocument1 pageColombia Check Stubwadealexus50No ratings yet

- 04.17.23 Article III Standing and Memo of LawDocument15 pages04.17.23 Article III Standing and Memo of LawThomas WareNo ratings yet

- Jacob Blake Criminal Complaint For Third Degree Sexual AssaultDocument4 pagesJacob Blake Criminal Complaint For Third Degree Sexual Assaultdiscuss100% (6)

- 2024 DFL State Convention Platform ResolutionsDocument12 pages2024 DFL State Convention Platform ResolutionsMark WassonNo ratings yet

- Republican State Convention AgendaDocument2 pagesRepublican State Convention AgendaMark WassonNo ratings yet

- Order - Dismiss - Not Stipulated, Entire CaseDocument4 pagesOrder - Dismiss - Not Stipulated, Entire CasePatch MinnesotaNo ratings yet

- Freeborn County AnswerDocument4 pagesFreeborn County AnswerMark WassonNo ratings yet

- Second Amended Criminal ComplaintDocument8 pagesSecond Amended Criminal ComplaintMark WassonNo ratings yet

- Warrant of CommitmentDocument2 pagesWarrant of CommitmentMark WassonNo ratings yet

- Mower County Attorney Letter Involving Police ShootingDocument3 pagesMower County Attorney Letter Involving Police ShootingMark WassonNo ratings yet

- LL & LW ProjectDocument21 pagesLL & LW ProjectadvikaNo ratings yet

- Roger Thomas Clark, Amended ComplaintDocument20 pagesRoger Thomas Clark, Amended ComplaintJoseph CoxNo ratings yet

- Checklist For EU GDPR Implementation enDocument3 pagesChecklist For EU GDPR Implementation enUsman HamidNo ratings yet

- Published United States Court of Appeals For The Fourth CircuitDocument9 pagesPublished United States Court of Appeals For The Fourth CircuitScribd Government DocsNo ratings yet

- Ethics NotesDocument8 pagesEthics NotesJames Glerry AaronNo ratings yet

- Universal Declaration of Human RightsDocument2 pagesUniversal Declaration of Human RightskrissyNo ratings yet

- Torture 2009Document163 pagesTorture 2009Achintya MandalNo ratings yet

- Western TimesDocument8 pagesWestern TimesmrfjollyNo ratings yet

- PaybackDocument222 pagesPaybackWasseem AtallaNo ratings yet

- Letter From National Immigration and Customs Enforcement Council To Members of CongressDocument6 pagesLetter From National Immigration and Customs Enforcement Council To Members of CongressEd O'KeefeNo ratings yet

- Bryan Norberg Lawsuit Vs Town of Bluffton (Re Former Bluffton Chief David McAllister)Document13 pagesBryan Norberg Lawsuit Vs Town of Bluffton (Re Former Bluffton Chief David McAllister)Island Packet and Beaufort GazetteNo ratings yet

- Cutting Through Biden's Illusions' - American ThinkerDocument4 pagesCutting Through Biden's Illusions' - American ThinkerRonNo ratings yet

- EEAS EU Cyber Diplomacy ToolboxDocument9 pagesEEAS EU Cyber Diplomacy ToolboxKarthikNo ratings yet

- Gender and Society Preliminary Exams: True or FalseDocument3 pagesGender and Society Preliminary Exams: True or FalseLyn ZubietoNo ratings yet

- Local Resident Killed by Train: Bid High On Big ThursdayDocument24 pagesLocal Resident Killed by Train: Bid High On Big ThursdaysurfnewmediaNo ratings yet

- Buffalo CP Report FinalDocument130 pagesBuffalo CP Report FinalAnji MalhotraNo ratings yet

- Contestaţia În Anulare, Între Trecut Şi Prezent, În Reglementarea Codului de Procedură Penală În VigoareDocument48 pagesContestaţia În Anulare, Între Trecut Şi Prezent, În Reglementarea Codului de Procedură Penală În VigoareRCNo ratings yet

- CRPC Internal 2Document11 pagesCRPC Internal 2SHRAAY BHUSHANNo ratings yet

- 25 06 15 I PDFDocument14 pages25 06 15 I PDFNathaniel LyngdohNo ratings yet

- Policing of SpainDocument9 pagesPolicing of SpainAxel Rose SaligNo ratings yet

- Global Initiative Against Transnational Organized Crime: Malgré La Fermeture Des Frontières, Le Marché Mauricien de La Drogue en Plein EssorDocument35 pagesGlobal Initiative Against Transnational Organized Crime: Malgré La Fermeture Des Frontières, Le Marché Mauricien de La Drogue en Plein EssorDefimediaNo ratings yet

- Juristic Act and ContractDocument29 pagesJuristic Act and ContractWISDOM-INGOODFAITHNo ratings yet

- Why Do I Need Cyber Liability InsuranceDocument15 pagesWhy Do I Need Cyber Liability InsuranceFanniNo ratings yet

- Rico Case Statement InstructionsDocument3 pagesRico Case Statement InstructionsJuliet LalonneNo ratings yet

- Digest CompilationDocument27 pagesDigest Compilationcm mayorNo ratings yet

- CrimproDocument10 pagesCrimproninya09No ratings yet

- Clean Copy of Obligations and Contracts Ateneo ReviewerDocument27 pagesClean Copy of Obligations and Contracts Ateneo ReviewerArnel Manalastas100% (1)

- OkumuraDocument3 pagesOkumuraJohn Winchester PalmonesNo ratings yet